![]()

To Our Valued Customers,

Welcome to the home stretch for 2022. It has been another year filled with a range of unexpected issues which have surfaced within our industry, country, and in many cases the world.

Transportation and freight continue to be a challenge with diesel fuel staying around $6 per gallon and a depletion in supply causing concern. Driver shortages continue to plague all industries reliant on over-the-road trucking.

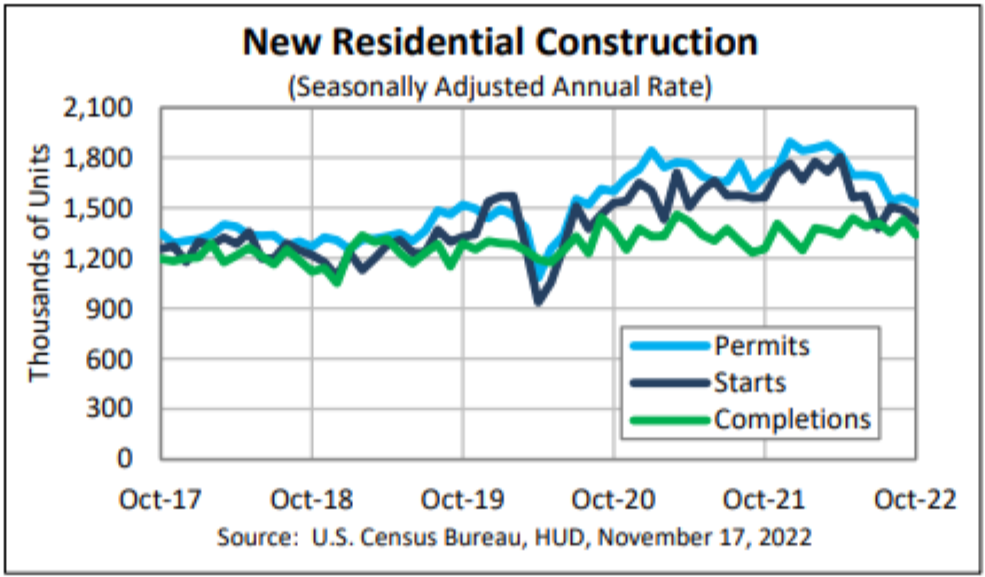

Single-family housing is under economic headwinds on many fronts. Mortgage Interest rates have risen quickly from under 3% to now sitting at north of 7%. These increases will surely continue to impact single-family housing permits, starts, and completions in nearly all markets. (Figure 1. U.S. New Residential Construction Trends). Supply chain issues have improved in the last six months for a range of building materials that were experiencing lengthy lead times earlier this year. There are still a few products that continue to be problematic. Labor shortages are prevalent in nearly all trades. Multi-family construction and commercial activity remain strong in most markets, however, the Architectural Billing Index (ABI), a clear indicator of demand for new non-residential projects, dropped to 47.7 in October after trending above 50 since February of 2021. While the lead time on commercial projects is significantly longer than single-family housing the same headwinds facing single family will likely impact commercial activity at some point in the future.

Figure 1. Current and Forecasted Construction in the U.S. (https://www.census.gov/construction/nrc/pdf/newresconst.pdf)

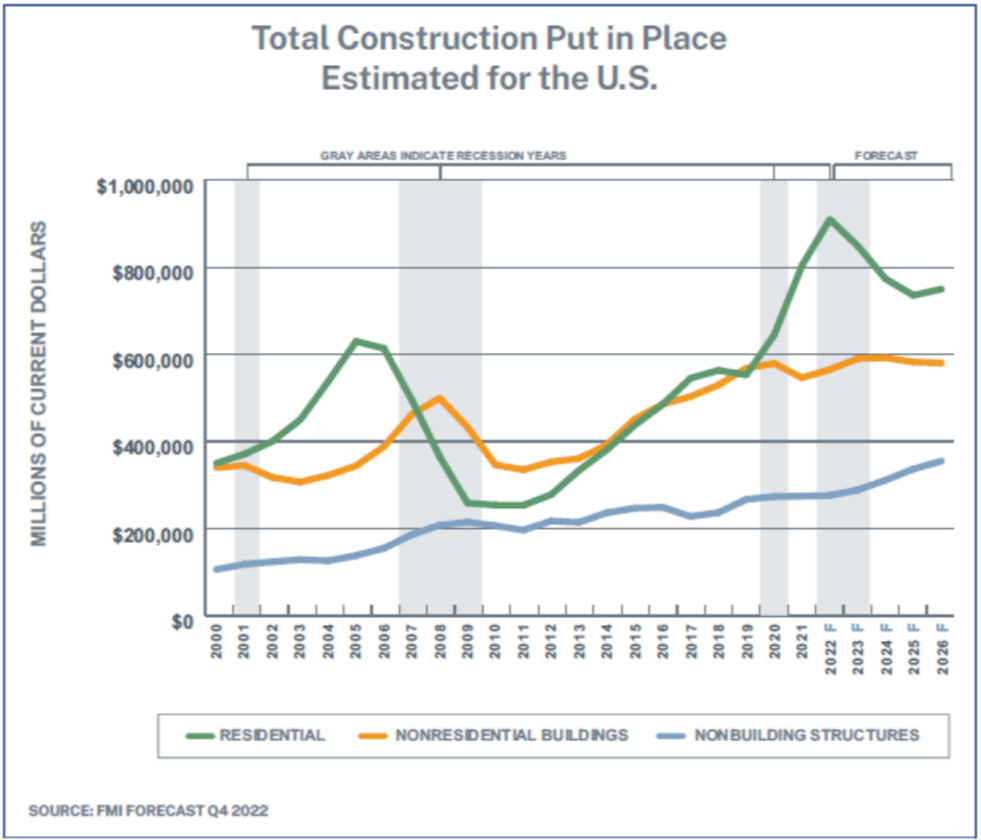

Figure 2. provides a useful summary view of the forecast for residential, non-residential, and non-building structures through 2026, including indicators for recession years. (FMI 2022 North American Engineering and Construction Outlook Fourth Quarter Edition, 2022).

Figure 2. Current and Forecasted Construction in the U.S.

Commentary By Major Product Category

Our view and outlook for the building materials industry by category for the end of 2022 and early 2023 are as follows.

Drywall – Most of the supply chain issues we have all experienced appear to be behind us, however one area still experiencing tight availability is the Southeast. Recently, a major drywall manufacturer notified us of a price increase, this could be a signal that others may follow. Glass-mat products continue to experience supply issues, primarily due to the limited availability of the facer component. We sense that glass-mat products will be in very tight supply throughout 2023. Wallboard pricing will moderate in 2023. We anticipate a first-quarter increase of around 10% to offset continued raw input increases, particularly in natural gas. The remainder of 2023 should see a very calm pricing environment.

Insulation – Availability has increased for insulation products. Fiberglass, mineral wool, and spray foam have all greatly improved shipping cycles in the last few months. Raw input costs, particularly natural gas, continue to cause prices to rise. Additionally, fiberglass and mineral wool increases have been announced for mid-December.

Joint Compound – Barring any unforeseen supply chain disruptions like the winter storm that struck the Houston metro area in 2021, joint compound should remain readily available throughout 2023. Drywall tape has been in short supply due to manufacturing issues and the major hurricane in Florida. This tightness in supply should be a short-term issue that will ease as we enter 2023.

Ceilings & Grid – Following unusually high increases in 2022, we expect pricing in this area to return to a normal cadence. Historically in this product category, a mid-single-digit increase in the first and second half of the year was typical. Our view is that 2023 will reflect a more historical pattern. Product availability is strong for this category.

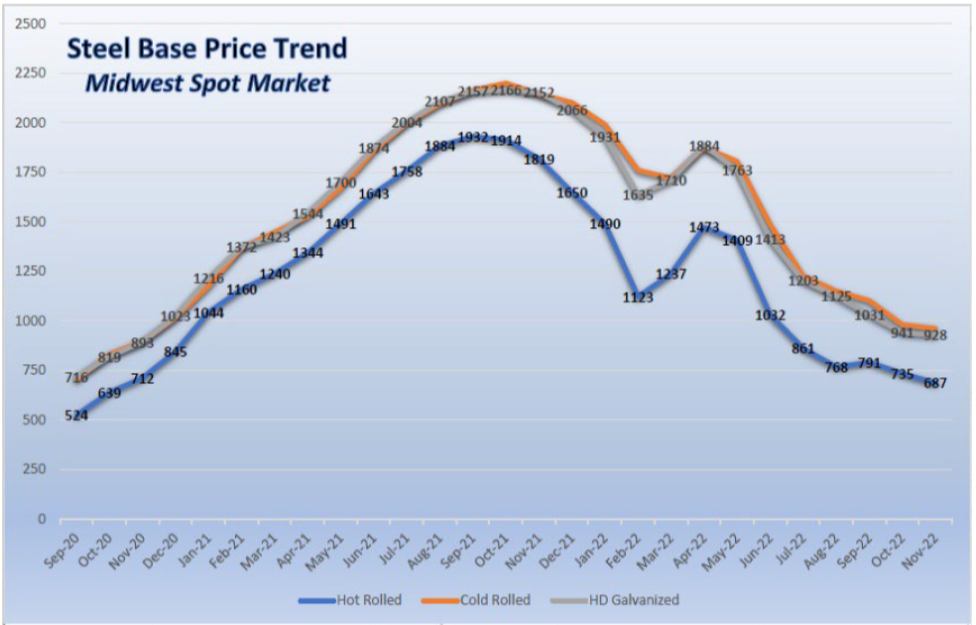

Steel – Supply chain issues were the root cause of this category’s rapid rise in 2021-2022. In 2023, we expect this to change to a pattern of price moderation. Increased worldwide availability combined with weakened demand for automotive and appliance categories will likely cause construction steel products to experience some deflation in 2023, with availability returning to a normal cycle. According to the American Iron and Steel Institute (AISI), domestic steel output was 1,688,000 net tons in the week ending Oct. 15, with utilization running at about 76%. Some softening is showing, in which rates above 80% utilization are considered strong, and rates at the peak of demand were running at 85% for a 3-month period. (Clark Dietrich, Domestic Market Update Nov. 22).

Figure 3. Base Steel Price Trends (Clark Dietrich, Domestic Market Update Nov. 22).

EIFS/Stucco – Lead times have returned to a more normal cycle for EIFS and stucco products. With this category being heavily involved in the commercial and multi-family sectors, we anticipate a price increase of around 10% in February.

These guidelines are our best attempt to help you understand what the future may hold. In no way are we able to guarantee what the future may bring. For example, the impacts in Florida associated with Hurricane Ian are a good reminder of how quickly a market can be disrupted by events beyond our control. We will strive to give you the most current information as we receive it.

Thank you for your business and continued support.

Sincerely,

Kirby Thompson

Chief Sales Officer