To Our Valued Customers,

We are nearly half of the way through 2023, and by most accounts, our industry is running at levels that have surprised many of us. Despite the headwinds forecasted for this year, we seem to be progressing well on several fronts. It seems like we are only one international incident away from an economic crisis. Let’s all hope that the world can avoid any unnecessary missteps.

While fuel costs have moderated recently, the diesel price index is still significantly higher than the five-year average price. The instability in a consistent energy policy has led to unstable prices from quarter to quarter. Driver shortages continue to be an issue in all parts of North America.

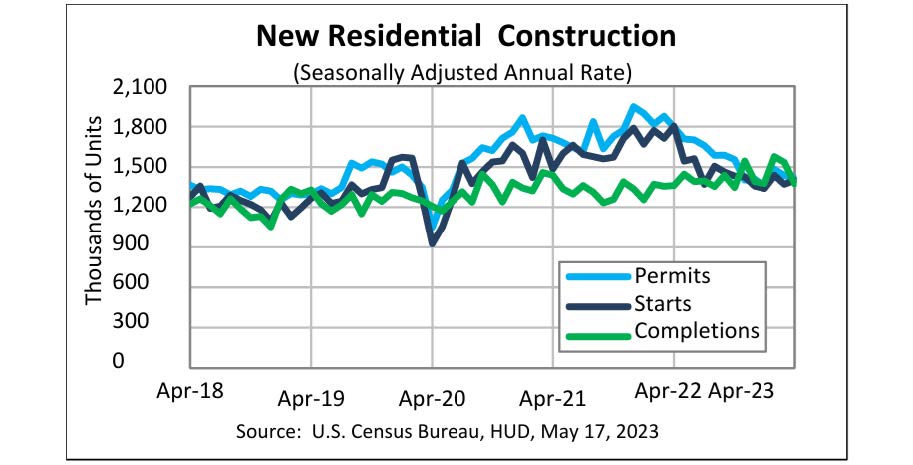

Single-family housing has borne the brunt of the economic headwinds. While down from the 2022 levels, we are all grateful that the current activity is a little better than the forecasts had predicted. Mortgage rates are hovering around 6.5%. The lack of housing inventory has kept the prices in most markets at very strong levels. Multi-family housing has been the most robust portion of our market. Despite gloomy forecasts for several years, this sector of the market remains very strong.

Figure 1. Current and Forecasted Construction in the U.S.

https://www.census.gov/construction/nrc/pdf/newresconst.pdf

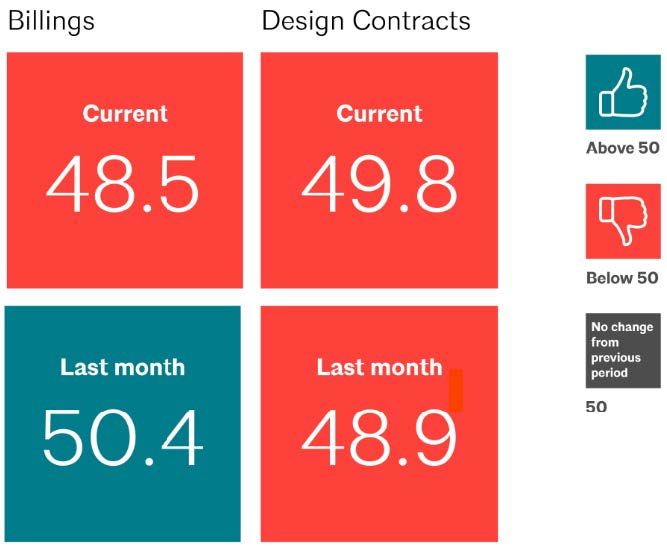

The commercial market has been very good for most parts of North America. A flurry of microchip manufacturing facilities, electric battery plants, and data storage centers has led the way for a strong showing in this market. The Architectural Billing Index (ABI) in April was 48.5 a slight decrease from March in which the ABI had come in at 50.4. The tenant improvement market continues to lag as many areas have not seen workers return to their offices.

Figure 2. Architectural Billing Index (ABI) April 2023

https://www.aia.org/pages/6630599-abi-april-2023-business-conditions-soften-

Commentary By Major Product Category

Here’s our take on the outlook for the remainder of 2023 by product category.

Drywall – The supply chain issues that plagued our industry in 2022 are finally in the rearview mirror. The southeastern portion of the United States was the last area to free up supply after battling the two hurricanes that impacted Florida in the fall. This market continues to experience the strongest demand and is forecasted to remain strong throughout the calendar year. The west coast and the Southwest have experienced some softness in their markets. The second half of this year is anticipating activity in these markets to increase. We expect the pricing for wallboard products to remain stable in most markets this year barring any unforeseen economic issues.

Insulation – Due to the closure of a major plant on the west coast, this industry is running at near capacity pace. Lead times have come down significantly since last year. Fiberglass batts and mineral fiber products are now readily available. Blowing wool products typically become tight in supply in the fall during the heavy reinsulating period. We expect pricing to remain stable in this product category for the remainder of this year.

Joint Compound – The supply chain has been restored to normal lead times. The drywall tape shortage that occurred last fall is now corrected, and the product is readily available.

Ceilings & Grid – Availability is not an issue with this product category. We believe we have returned to a traditional price increase cadence of one increase in the spring and one increase in the fall.

Steel – This product category has shown the most volatility of any category in our business. The effects of worldwide events and import tariffs have been seen with steel products. We saw the prices rise significantly more than other categories in 2022 and we’ve now seen them decline more than any other product category so far this year. We do believe that pricing will be mostly stable at the current levels for the remainder of 2023.

EIFS/Stucco – Lead times have returned to normal levels in this category. The cement industry is experiencing some shortages. As a result, there is a price increase announced for July 1, 2023, for stucco and cementitious products associated with stucco. One stucco manufacturer has left the industry in Florida. Given the robust opportunity in Florida, there may be some shortages for a short time while the remaining three suppliers absorb that business.

These guidelines are our best attempt to help you understand what the future may hold. In no way are we able to guarantee what the future may bring.

In closing, I’d like to say how pleased we are that on March 31, 2023, we were successful in acquiring Marjam. This acquisition will greatly strengthen our position from New England to Florida along the eastern seaboard. We are also extremely excited about the increased activity on our Ecommerce site MyFBM.

Thank you for your business and continued support.

Sincerely,

Kirby Thompson

Chief Sales Officer